2018 has been a year of mixed fortunes for house prices across the UK, according to the latest Asking Price Index from Home.co.uk, which covers December.

House prices fell in England’s three most populous and expensive regions in December, the report reveals.

2018 saw the South East and East of England property markets slide into the red, following in the footsteps of long-suffering Greater London. House prices in the capital have now been on a downward trend for 31 months, and, during this time, the mix-adjusted average property value has fallen by 6.3%.

The impact of the downturn on both the South East and East of England on the national average has been dramatic, taking annual growth from“just about keeping pace with inflation” to “seriously sub-inflation” during the course of the year.

In fact, when compared to the Retail Price Index (RPI) growth in England and Wales, house price inflation has been negative in real terms for 22 months.

The South West looks like the next region to slip into the red. House prices have dropped in five out of the last six months, with the current average annual growth standing at just 0.7%.

Similarly, Home.co.uk expects the East and West Midlands markets to cool off during 2019, with consequential price erosion to follow; nothing catastrophic, nor a consequence of Brexit, merely a natural post-boom rebalancing of supply and demand.

A far cry from the doom and gloom in the South East and East of England, 2018 has been a good year for the North, West and Wales. Inflation-beating price growth is still evident in Yorkshire (+4.7%), the North West (+4.8%) andWest Midlands (+5.2%), as their respective regional property markets continue to thrive.

Wales remains the leader of house price growth, with annual gains amounting to an average of 7.4%.

For the time being, property marketing times are still falling rapidly, and Home.co.uk expects this late-cycle boom to roll on throughout 2019.

Overall, the supply of properties for sale in the UK has risen by 3%, while the total stock has increased by 10.8% year-on-year.

In December last year, house price growth across the UK stood at an average of 2.6%. The same measure today is just 0.8% and continues to trend downwards.

Property market activity fell further in November, according to the latest UK Residential Market Survey from the Royal Institution of Chartered Surveyors (RICS).

The results of the survey are consistent with a weaker trend in housing sales market activity, with headline indicators on both demand and supply slipping further into negative territory.

Furthermore, forward looking metrics suggest that momentum is likely to continue dropping in the coming three months, although a somewhat stable trend is expected to emerge further ahead.

Housing demand

Starting off with housing demand, the RICS new buyer enquiries gauge fell to -21% in November, from -15% in the previous month. This represents a more cautious approach from property buyers.

The latest figures continue to suggest that the limited choice of properties for sale is likely to be one factor hampering buyer demand.

The new instructions series pointed to a decrease in the supply of properties coming onto the market for the fifth consecutive report.

Significantly, the net balance of -24% in November was the fastest pace of decline in new sales listings noted in 28 months. As a result, average housing stock levels on estate agents’ books remained close to record lows, at 42.1.

Property sales

At the same time, contributors continue to report that new appraisals by property valuers are down in comparison to a year earlier, suggesting that any pick-up in new sales listings is not on the horizon.

Meanwhile, the time taken to complete a sale from initial listing stands at approximately 19 weeks. As such, this represents the longest duration since the series was first introduced in February 2017 and is another sign of challenges in the sales market.

Property Market Activity Falls Further, the RICS Reports

Against this backdrop, the newly agreed sales net balance moved to -15% from -10% in the previous report, pointing to a modest drop in sales transactions nationally. When disaggregated, activity was reportedly subdued in almost all areas of the UK.

Anecdotal evidence continues to suggest that Brexit uncertainty and a lack of fresh stock onto the market are the main factors behind the slowdown in activity.

Moreover, there is little sense that these headwinds will fade anytime soon. Headline sales expectations fell to -23% in November (from -6% previously), indicating that momentum looks likely to slip further over the coming three months.

That said, contributors are expecting sales volumes to stabilise in the coming year, with positive sales trends envisaged across Northern Ireland, the South West and East Anglia in particular.

House prices

Looking at house prices, the headline price net balance came in at -11% in November, which is broadly unchanged from -10% in October. Overall, this indicator is consistent with a modest fall in property values nationally.

Still, the regional picture remains highly varied, with negative price trends across London, the South East and East Anglia contrasting with solid price growth reported in Northern Ireland, Scotland, the Midlands and North West.

Looking ahead, price expectations for the coming three months dipped to -25% (from -17% in October), which is consistent with a decline in national house price growth on a UK-wide basis. The 12-month outlook, however, is broadly flat.

Lettings market

In the private rental sector, the latest figures are indicative of demand from prospective tenants holding broadly steady for the second consecutive month.

Alongside this, the new landlord instructions series remained entrenched in negative territory (net balance of -14%), signalling a decline in the supply of fresh rental stock coming onto the market.

As a result of these dynamics, rent prices are expected to rise modestly over both the three and 12-month horizons.

Further ahead, rent price growth is expected to outpace that of house prices. On average, rents are predicted to rise by 3.1% per year over the next five years, while house price projections stand at an average of 2.3% on the same basis.

Steve Seal, the Director of Sales & Marketing at Bluestone Mortgages, comments on the report: “RICS continues to show that strains within the market are not exclusive to London, nor the south, as some may assume. With the current environment, there is a lot of uncertainty, and many buyers are choosing to wait until the New Year before making the biggest financial decision of their lives.

“As political uncertainty looms, borrowers need to be reassured that affordable lending can still be accessed. For those who are concerned about their finances moving into the New Year, getting in touch with a mortgage broker is a good place to start. Those with credit blips or with irregular incomes may fear that homeownership is unachievable, but there are lenders out there to help.”

Most tenants in the UK believe that they’ll never get a foot onto the property ladder, due to the high cost of saving for a deposit, according to a survey of 2,000 renters, commissioned by Intus Lettings.

56% of respondents said that they choose to rent their home because they can’t afford the initial lump sum of purchasing a property, which is up by 4% on last year.

This comes despite predictions that UK rent prices are expected to climb by 15% over the next five years, with house prices seeing the largest November drop since 2012 this year.

The research reveals that the issue of affordability is far more prevalent in over-25s, with some respondents even stating that the only way that they’d be able to buy a home is by winning the lottery.

While 57% of 18-24-year-olds have a more optimistic outlook on homeownership, those over the age of 25 continue to rent because of financial concerns, with 25-34-year-olds (63%), 35-44-year-olds (64%) and 45-54-year-olds (60%) all saying that they don’t have the money for a deposit. These figures are all up year-on-year.

The Lettings Manager at Intus Lettings, Hope McKendrick, says: “Despite wages rising at the fastest pace in nearly a decade and falling house prices, the difficulty of moving from rented accommodation to owning a property continues to be widespread.

“The problem offinding a deposit is a common theme across the regions. However, more people in Northern Ireland (69%), the South East (64%), South West (61%) and Wales (60%) have admitted they rent because they can’t afford to buy.”

When asked what the biggest factor was when looking for a property, 41% of tenants rated affordability as the biggest influence, with location (25%) and transport links (8%) ranking much lower.

McKendrick adds: “What the research does show is there is greater confidence amongst under-25s when it comes to owning a property in the future, compared to their older counterparts, with 75% of 18-24-year-olds saying they would save their own money to buy a property.”

This is up by 6% on last year’s survey results, with fewer tenants choosing to rent because it suits their lifestyle, which is down by 8%.

The Scottish equivalent of Stamp Duty, Land Buildings Transaction Tax (LLBT), could be raised to 4% for those buying additional properties north of the border.

On Wednesday (12th December), the Scottish Finance Secretary, Derek Mackay, proposed a 1% hike on the tax payable when purchasing buy-to-let properties or second homes.

Mackay set out his plans for tax and spending for the year ahead at Holyrood, as part of the Scottish Budget, which included the proposal to increase the surcharge on LLBT for additional properties from 3% to 4%.

If the Scottish Government approves the proposal, the rate hike will be introduced from 25th January 2019.

However, the 4% surcharge will not apply if the contract for a property transaction was entered into before 12th December 2018.

The proposed hike would mean that a buy-to-let landlord purchasing a property in Scotland for £250,000 would see their LLBT bill increase from £9,600 to £12,100.

Several property experts have expressed their concerns over the adverse effect that LLBT is having, following its introduction in April 2015, especially on the middle to upper end of the Scottish property market.

There is also plenty of evidence to suggest that LLBT is placing upward pressure on rent prices, as Brian Moran, the Lettings Director at Your Move Scotland, explained back in June: “Rents are rising rapidly as a result of the LLBT surcharge for buy-to-let properties.

“This tax hike has dissuaded landlords from investing in the sector, leading to a shortage of homes to rent, compared to the demand for housing.”

He continued: “With the limited supply of rental properties, potential tenants have been forced to compete to secure homes, pushing up rents.

“The introduction of this anti-landlord legislation from Holyrood has ensured the cost of the policy has hit tenants hardest.”

Landlords must note that the Scottish LLBT is separate to the 3% Stamp Duty surcharge introduced by the Government back in April 2016.

Landlord gains from shopping around for keenly priced buy-to-let mortgage rates could be wiped out by hefty product fees, according to the latest Mortgage Tracker from online broker Property Master.

The Mortgage Tracker report has been compiled every month since January this year, but this is the first time that Property Master has assessed average product fees.

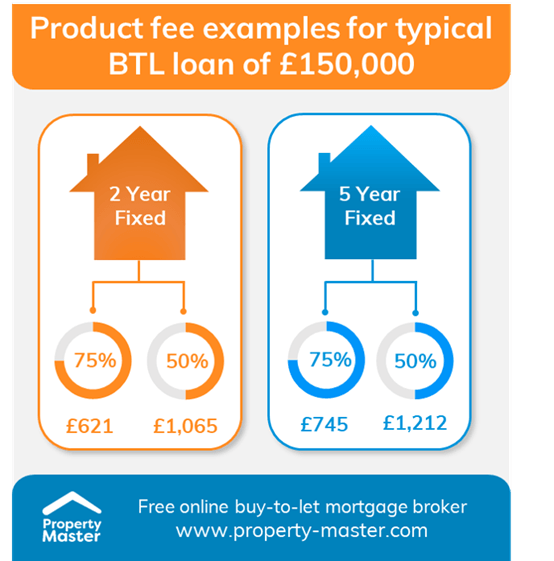

The research found that these could range from a one-off charge of £621, up to £1,212.

According to the Mortgage Tracker, the average product fee on a two-year fixed rate buy-to-let mortgage for a typical amount of £150,000, with a 75% loan-to-value ratio (LTV) was £621. This rose to £1,065 on an LTV of 50%.

The average product fee for a five-year fixed rate deal for the same amount, at 75% LTV, was £745, jumping to £1,212 at 50% LTV.

Landlord Gains from Best Mortgage Rates Could be Wiped Out by Product Fees

Property Master’s Mortgage Tracker follows a range of buy-to-let mortgages for an interest-only loan of £150,000. Deals from 18 of some of the biggest lenders in the buy-to-let market, including Barclays, BM Solutions, RBS, The Mortgage Works, Godiva, and Precise, were tracked.

Figures for this month’s Mortgage Tracker were calculated on deals available on 1st December 2018.

Angus Stewart, the Chief Executive of Property Master, says: “Understandably, landlords will be attracted to the headline rates lenders quote, but it is important also to factor in additional costs, in particular, product fees. Landlords may also find other fees going under other names, such as an application fee, or a booking fee, or an account fee. When shopping around, landlords need to make sure they have the full facts and the total cost in front of them.

“With further rate rises on the horizon, coupled with a range of increased regulator and tax costs, landlords are becoming more aware than ever of the need to watch their finances. There are certainly good deals out there, but make sure you know all the costs involved before signing a new finance deal.”

Landlords, have you been caught out by product fees?

A competitive market has caused the highest rate of remortgaging for a decade, according to UK Finance’s Mortgage Trends Update for October 2018.

Some 50,500 new homeowner remortgages were completed in the month of October, which is up by 23.2% on the same month last year. The £9.2 billion of remortgaging was 22.7% higher year-on-year.

32,900 new first time buyer mortgages completed in October, some 8.2% more than in the same period of 2017. This £5.5 billion of new lending was 12.2% higher on an annual basis.

UK Finance found that the average first time buyer was 30-years-old and had a gross household income of £42,000.

There were 33,400 new home mover mortgages that completed in October, which is 4.0% more than in October last year. The £7.4 billion of new lending in the month was up by 8.8% year-on-year.

The average home mover was 39-years-old and had a gross household income of £56,000.

6,100 new buy-to-let property purchase mortgages were completed in the month of October, which is down by 9.0% on the same month of 2017. By value, this £0.8 billion of lending was down by 20.0% annually.

There were 15,700 new buy-to-let remortgages in October, some 5.4% more year-on-year. This £2.5 billion of lending was up by 4.2% on October last year.

Competitive Market Causes Highest Rate of Remortgaging in a Decade

Comments

Jackie Bennett, the Director of Mortgages at UK Finance, says: “Remortgaging has reached its highest level in almost a decade, as homeowners take advantage of a competitive market and lock into attractive deals. This also reflects the large number of fixed rate mortgages coming to an end, which is expected to continue into 2019.

“There has been relatively strong growth in the number of first time buyers, with schemes such as Help to Buy providing vital support to those getting a foot on the housing ladder.

“Meanwhile, the buy-to-let market has seen a continued increase in remortgaging and a softening in home purchase activity, in line with ongoing trends in recent months.”

The Founder of CashbackRemortgages.co.uk, Suchit Sethi, also comments: “This explosion in remortgaging activity is yet more proof that homeowners are taking concerted action in the face of Brexit-related uncertainty.

“These are the strongest remortgaging figures in a decade, which is understandable, given that we are on the cusp of one of the biggest politico-economic events for a decade in Brexit.

“Fortunately, the mortgage market is still flush with attractive deals for discerning borrowers. Rates may no longer be as low as they were, but they are still extremely competitive.

“The threat of a rate rise as soon as May is likely to have lit a fire under the sector, too, with homeowners scrabbling to lock into competitive deals while they still can.

“The resilience of the first time buyer is also very encouraging. Help to Buy has had a huge impact on younger people struggling to get onto the ladder, while the retreat of landlords has been the icing on the cake.

“These figures offer some reassurance that homeowners are taking the appropriate steps to protect themselves, even while the political establishment looks set to tear itself apart.”

John Phillips, the Group Operations Director at Just Mortgages and Spicerhaart, gives his thoughts on the figures: “Today’s UK Finance Mortgage Trends report reveals the highest rate of remortgaging in a decade, with a rise of 23.2% on last year, confirming that remortgaging is the clear driving force in the mortgage market at the moment. Last month’s estimate showed a downturn in remortgaging, and I was quite surprised, as it was not what we have been seeing at Just Mortgages. These figures are much more of a reflection of what we are seeing in the market.

“We can also see that home mover mortgages are up, too, perhaps signalling that now the initial reluctance to move amidst Brexit uncertainty is straight to waive slightly. There will probably be another dip in home mover activity as we go into 2019, but I think remortgaging will remain strong. There are lots of fixed rate deals coming to an end, and people are keen to lock in good fixed rate deals now, before potential rate rises.

“Also in tougher times, when purchasing is down, lots of brokers start to focus more on their remortgaging business, which they should be doing anyway, and that has almost certainly impacted on the rise.”