In the last quarter (Q4) of 2018, 40% of the UK housing

stock was private rental, increasing to 50% in cities such as Newcastle upon

Tyne and Manchester, according to a new report from TwentyCi.

The marketing consultancy’s Property & Homemover Report

for Q4 reveals a steady increase in the percentage of rental properties

available over the previous 12 months.

However, the study confirmed an overall property market

slowdown in 2018.

Despite a 4% rise in new instructions year-on-year in Q4,

there was a 1.2% decline in exchanges, with 20% of property sales falling

through, which might explain why rental stock has increased.

Overall, the data suggests that the north-south divide is

very much still in existence, despite higher salaries in the south. For example,

the 25% of highest earners in London will be spending between 40-60% of their

take-home pay on their mortgage to buy a home of equal standing with a 40%

deposit.

Meanwhile, the 25% of lowest earners in the capital would

not be able to afford to buy a property of equal standing, as it would mean

spending between 70-131% of their take-home earnings on their mortgages.

For the lowest earners, the cost of renting a property of

equal standing would be between 57-90% of their take-home pay.

However, the figures show that there are many locations in

the Midlands and north of England where the 25% of lowest earners can afford to

rent or buy.

In Nottingham, for instance, to rent a home of equal

standing would cost 35% of take-home pay, while buying with a mortgage would

eat up 37% of take-home earnings.

Colin Bradshaw, the Chief Customer Officer at TwentyCi, says: “Q1 2019 and the

outcome of the Brexit process will determine the outturn for the next 12 months.”

With such

a high proportion of private rental properties in the UK housing stock, demand

from tenants looks set to remain high.

Regardless of how favourable the market was when you purchased your buy-to-let property, it still represents a significant investment with the aim of providing you with a steady rental income and an increase in capital value over the long-term.

Having made that financial commitment, it is therefore highly likely that you want to do everything you can to protect your investment. Some of these risks may be more obvious than others.

Insurance

Adequate landlord insurance cover is essential to protect your rental property from major risks that could render it uninhabitable or, worst case scenario, require it to be rebuilt completely. Both would result in a loss of rental income. This could be fire, storm damage, flooding or vandalism.

Building insurance protects the structure and fabric of your property (the actual building) and the cover needs to be sufficient to replace the property if it was sufficiently damaged to require rebuilding. If you’re not sure if your buildings insurance provides high enough cover, carry out a valuation using the Royal Institution of Chartered Surveyors online cost calculator. Bear in mind that not all buildings insurance cover includes subsidence as standard, so you may want to add this to your policy.

Your tenants are responsible for arranging their own contents insurance cover, but you may also have some of your own possessions in the property, such as furnishings, fittings and equipment that are at risk of damage, loss or theft, which you may wish to protect against.

There are also other, less tangible, threats – such as compensation claims – which you may wish to insure yourself against, should tenants allege you have in some way failed in your duty of care as the landlord of the property. Landlords’ liability insurance is intended to indemnify you against any such claims.

If your property is going to be empty for any period of time, either due to inoccupation or renovation, then check you’re still covered by your insurance policy – many will stipulate certain conditions relating to required security measures, or the length of time the property is vacant, beyond which you may no longer be entitled to compensation.

Security

As important as landlord insurance is, there are a host of

ways in which you can look after your rental property and ensure it is well

looked after, to minimise the likelihood of having to make a claim.

Protecting your property against theft and intruders

requires constant vigilance – particularly when it comes to securing access and

maintaining alarms and locks.

Even if you have landlords insurance, as the insured party, you are responsible to minimising the risks to your investment property. If you don’t, then, in the event of an insurance claim, you may find yourself receiving a reduced – or worse, no – compensation payment as a result of your negligence.

Protecting your Investment Property, by SafeSite

Michael Knibbs, the Managing Director of SafeSite Security Solutions cautions: “If your property is unoccupied for any period of time, or undergoing renovation or building work, this may increase its vulnerability. You may want to consider more robust security measures, such as timber or steel hoardings for doors and windows, or security fencing if you have a larger perimeter to secure.

“Don’t forget about any outbuildings, such as garages or sheds. These also need to be kept secure, either with a sufficient locking system or with bolts and padlocks. Consider storing any valuable items off site if the property is standing vacant.”

Security cameras offer a dual benefit – they provide a visible deterrent and help you to monitor any suspicious activity, as well as providing the evidence should you need to seek a prosecution.

Indoor and outdoor lighting is one of the easiest ways to deter criminals. Keep hallways and stairwells lit, and replace any burnt out bulbs immediately. Motion activated lights illuminate driveways and gardens, and are a useful intruder deterrent, as burglars certainly don’t want to be caught in the spotlight.

Tenant checks

It may sound obvious, but your tenants are key to the success of protecting your investment property – not just in terms of ensuring you have carried out sufficient credit checks to guarantee your monthly rental payments, but also in terms of their personal responsibility in looking after the property while they are living there. As a landlord, you are entitled to expect that your tenants treat your property with due care and attention.

Making sure you choose the right tenants from the outset

using the best checking mechanisms – whether you’re doing this yourself or

through a letting agency – is an important part in ensuring your investment

property is in the right hands.

This includes seeking and securing financial and personal references, as well as proof of identification, and legal right to rent checks. Depending on how the tenant is intending to cover their rent, you may also want to see proof of employment or confirmation from the agency providing benefits.

Following these measures will help ensure your tenants enjoy their new home, and give you peace of mind that your property is safe, secure and in good hands.

London house prices are set to begin a recovery this year,

due to booming rental yields in some boroughs, according to analysis by Home.co.uk.

The property website expects the slump in the capital’s

housing market to come to an end in 2020, thanks to improving rental yields

making property more attractive to investors.

Home’s data suggests that this recovery is likely to begin

in Newham, where, in December 2018, the average rental yield was 4.9%, compared

to 3.6% in the same month of 2017. This 1.3% increase is the greatest rise in

any London borough, apart from the City of London, where a 1.5% increase was

observed.

The average rent price is Newham was £1,671 at the end of

last year, which is up by 7.6% on December 2017.

The next hotspot for investors is set to be Hammersmith

& Fulham, where the average rental yield rose by 1.2% over the year to

December, from 3.9% to 5.1%. This promising increase comes amid growth of 6.2%

in rent prices in this west London borough over the same period.

Other emerging areas for investors include Hackney and

Southwark, where yields increased by 0.7% between 2017-18.

Outside of the City of London, Southwark recorded the

greatest uplift in rents over 2018, at an average of 20.2%. A typical monthly

rent price in this borough was £2,532 in December.

A 0.6% rise in yields was recorded in the City of

Westminster and Tower Hamlets in the year to December last year.

Rents in Westminster increased by an average of 12.1% in the

12 months to December, taking the typical monthly price to £5,505, while rent

prices in Tower Hamlets grew by 10.1%, to £2,350 per month.

Housing market recovery is set to take longer in many outer

London boroughs, according to Home.

In Hounslow, Hillingdon, Harrow, Croydon, Waltham Forest,

Richmond upon Thames, and Barking and Dagenham, rental yields remained

unchanged between 2017-18.

Enfield, in north London, was the only borough to experience

a decline in rental yields over the same period, of 0.2%.

The Director of Home, Doug Shephard, says: “You just can’t

ignore the London property market’s remarkable ability to bounce back. History

has shown us time and time again how the UK’s leading property market can burst

back into growth after a period of correcting prices. The rate of rental yield

rises is surely the best analytical tool to pinpoint where the first green

shoots will emerge.

“Whilst it is encouraging that 32 out of 33 London boroughs are showing

increased yield year-on-year, it is where they are growing most quickly that is

of keen interest to investors. When they approach 6% in 16 or more boroughs,

demand in the London sales market will reignite.”

Are you more inclined to invest in the London property

market, now that it is due to recover?

Landlords across the country are being warned about failing

to comply with both selective and statutory licensing schemes.

There is growing concern in Reading that thousands of

landlords could soon face enforcement action if they do not sign up to a new

statutory licence, with the deadline less than two weeks away.

Under the new rules, mandatory HMO licensing has been

extended to almost all HMOs that are occupied by five or more people, where

there is sharing of some facilities. It is expected to affect more than 160,000

properties.

The licensing scheme was previously restricted to properties

that were three or more storeys high.

The change means that councils can now take further action

to clamp down on the small minority of landlords that let substandard or

overcrowded homes.

However, Reading Borough Council is concerned that many

landlords in the area are ignoring the new rules, with the deadline to apply

for a licence fast approaching.

The Council believes that just 135 of an estimated 3,000

landlords in Reading have signed up to the new licences.

Councillor John Ennis says: “Anecdotal evidence suggests that some landlords are reducing

the number of tenants in their property to avoid licensing.”

Reading

Borough Council rejected the Government’s decision to not allow a grace period,

giving landlords until 31st January 2019 to submit their

applications. Any landlord that fails to apply by the end of the month will be

subject to enforcement action.

At the same

time, Barnet Council is planning to introduce a stricter licensing scheme

designed to crack down on rogue landlords across the north London borough.

The Council

wants to replicate selective licensing schemes that are in force in other

areas, with prosecution or a civil penalty of up to £30,000 for those that fail

to comply with the scheme’s conditions.

Just over a

quarter (26%) of households in the borough were private tenants in 2016, which

is up from 17% in 2001. This is why Barnet is far more focused on stamping out

substandard housing and improving conditions in the borough.

Speaking at a meeting of

the Housing Committee last week, Chairman Councillor Gabriel Rozenberg, said: “In Barnet today,

the Conservatives are standing up for private renters. This new agenda

comprises stricter licensing controls and proposals for tougher enforcement. We

are putting tenants at the heart of our borough.”

It is

understood that the Council will hire additional members of staff to

investigate the viability of selective licensing in the borough, as well as

conduct extra housing enforcement and HMO licensing activities.

Landlords,

remember to check whether the areas that your properties are in are subject to

licensing schemes.

The current housing market outlook for the next three months

is the worst for 20 years, according to the latest study from the Royal

Institution of Chartered Surveyors (RICS).

A net balance of 28% of RICS members expect property sales

to fall in the next three months.

This is the most downbeat reading since the records began in

October 1998, with the pessimism blamed on the lack of clarity around Brexit.

A lack of housing supply and affordability also continued to

affect the market.

Sales expectations for the coming three months are now

either flat, with no change predicted, or negative, indicating a decline in

sales, across all parts of the UK, the report states.

Increasing numbers of surveyors reported seeing house prices

fall rather than rise in December, with a net balance of 19% witnessing

declines, rather than growth.

This is up from a balance of 11% in November, and marked the

fourth consecutive month of negative house price readings.

New buyer inquiries dropped for the fifth month in a row last

month, too.

The drop-off in interest from buyers was matched by a

decline in fresh properties coming onto the market.

The supply of new properties has been dwindling for six

months, Simon Rubinsohn, the Chief Economist at the RICS, says.

“It is hardly a surprise, with ongoing uncertainty about

the path to Brexit dominating the news agenda, that, even allowing for the

normal patterns around the Christmas holidays, buyer interest in purchasing

property in December was subdued.

“This is also very clearly reflected in a worsening trend

in near-term sales expectations.”

The latest official Office for National Statistics (ONS) house

price data suggests that housing activity has been muted recently, due to

Brexit uncertainty.

Looking further ahead, surveyors were a little more hopeful in

their sales expectations for 12 months’ time.

Rubinsohn says: “Looking a little further out, there is

some comfort provided by the suggestion that transactions nationally should

stabilise as some of the fog lifts, but that moment feels a way off for many

respondents to the survey.

“Meanwhile, it is hard to see

developers stepping up the supply pipeline in this environment.”

He added that getting close to Government

housebuilding targets would “require significantly greater input from

other delivery channels, including local authorities”.

Students are overpaying for their accommodation in most UK

university cities, according to new data from Mojo, an online mortgage broker.

The study found that those in Exeter, Norwich and Newcastle

are the worst affected.

This January, university students will be looking to secure

their accommodation for the next academic year. For many students, it’s

important that they find the perfect property, in a prime location, for a

reasonable price.

However, students in some university cities could be forking

out a lot more money for their accommodation, simply because they used a

dedicated student letting agent.

Mojo compared the prices of rental homes listed on property

portals, such as Rightmove, Zoopla and Prime Location, to those by specific

student letting agencies.

Specifically, it looked at more than 30 four-bedroom, fully

furnished houses in the most populated student areas of 19 UK cities.

Generally, Mojo found that it was more expensive to use a student-specific

service.

Students in Exeter fared the worst, overpaying by an average

of £69 per person if they rented via a student letting agent. In close second

and third places were Norwich and Newcastle, where students could be shelling

out £62 and £59 more than they need to every month respectively.

Average cost per

student, per month

Students are Overpaying for Accommodation in most University Cities

In total, Mojo found that rents were at least £10 greater on

student letting agents’ websites than property portals in nine cities.

Houses on Rightmove in Bristol and Bournemouth, however,

were actually £40 and £28 more expensive that on student letting agents’

websites respectively. Nevertheless, these two cities seem to be anomalies,

with the majority of student letting agents charging higher rents than local

estate agents using Rightmove.

The broker also found the most expensive areas to rent a

student property in the UK.

Most expensive

student areas

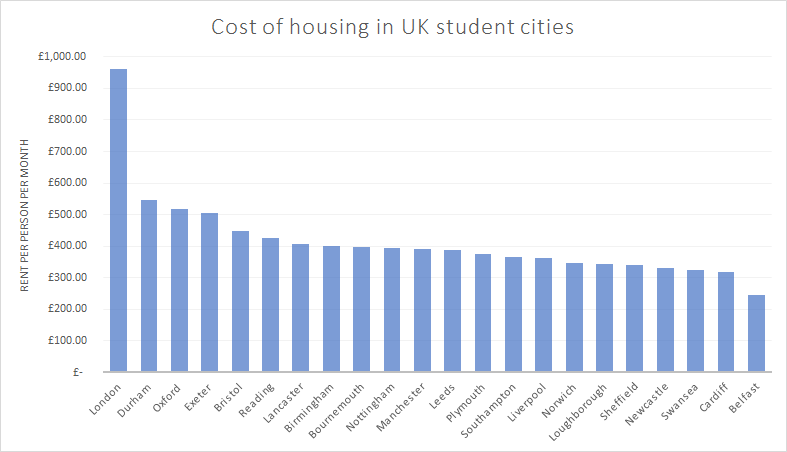

Unsurprisingly, London came out on top, with students in the

capital paying £961 per month on average. Next in line was Durham, at £546 a

month. Oxford and Exeter were close behind, at an average of £519 and £507

respectively.

Belfast boasts the cheapest student houses, at less than

half the price of the top three – an average of £246 per month. Students in

Wales can also take advantage of affordable rent, with the average monthly

price in Cardiff sitting at £319, while Swansea’s is £324.

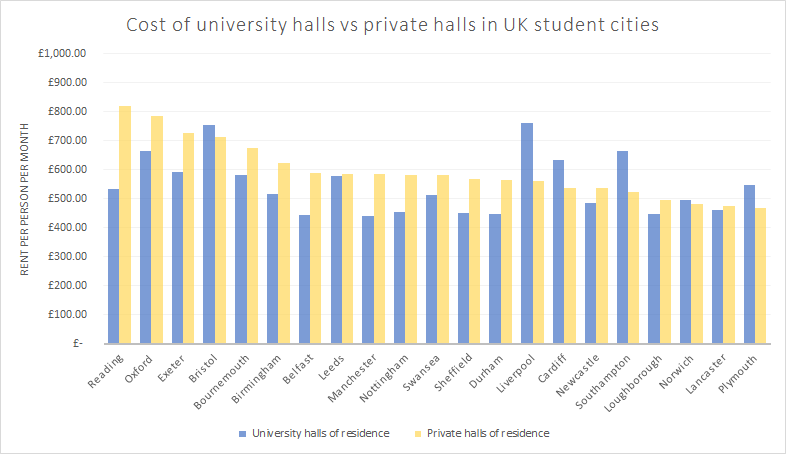

University or private

halls?

Mojo compared the price of living in halls owned by the

university, compared to those that are privately owned.

It found that most private halls of residence are more expensive than university-owned halls. In Reading, the average room in private accommodation will cost students £286 more on average than the university’s halls.

In fact, private accommodation costs up to three times more

than university halls in eight other cities. However, in some locations,

renting a room owned by the university will not be your cheapest option.

In Liverpool, Southampton and Cardiff, students can rent a

room in private accommodation for an average of £100 less per week than

university halls.

Top tips for student

accommodation

Mojo has put together some top tips for students, following the results of its findings:

Look for a property on a portal, as well as a

student letting agent, to find the best deal possible.

If you find a property that you like on an

agent’s website, then double-check whether it’s listed on a portal, as you can

sometimes find the same property for less.

If you find your perfect property through a

letting agent, take note of its features and run those through a portal’s

search feature – you could find a cheaper property with the same

specifications.

If you want to stay in halls, make sure to

compare the price of private and university accommodation, as the price varies

greatly depending on what kind of room you’re looking for.